Menu

- Home

- About Us

- Consular Services

- Culture

- Scholarships

- Media

- RTI

- Economic & Commercial

- Contact Us

Transparent Taxation - Honoring the Honest

Hon’ble Prime Minister Shri Narendra Modi will be launching on Thursday, the 13th August 2020 a platform for “Transparent Taxation - Honoring the Honest” aimed at bringing about major reforms in tax administration. The event will be witnessed by various Chambers of Commerce, Trade Associations, Chartered Accountants' associations as also eminent taxpayers, apart from the officials of Income Tax Department. Union Minister of Finance and Corporate Affairs, Shrimati Nirmala Sitharaman and Minister of State for Finance and Corporate Affairs, Shri Anurag Singh Thakur will also be gracing the occasion.

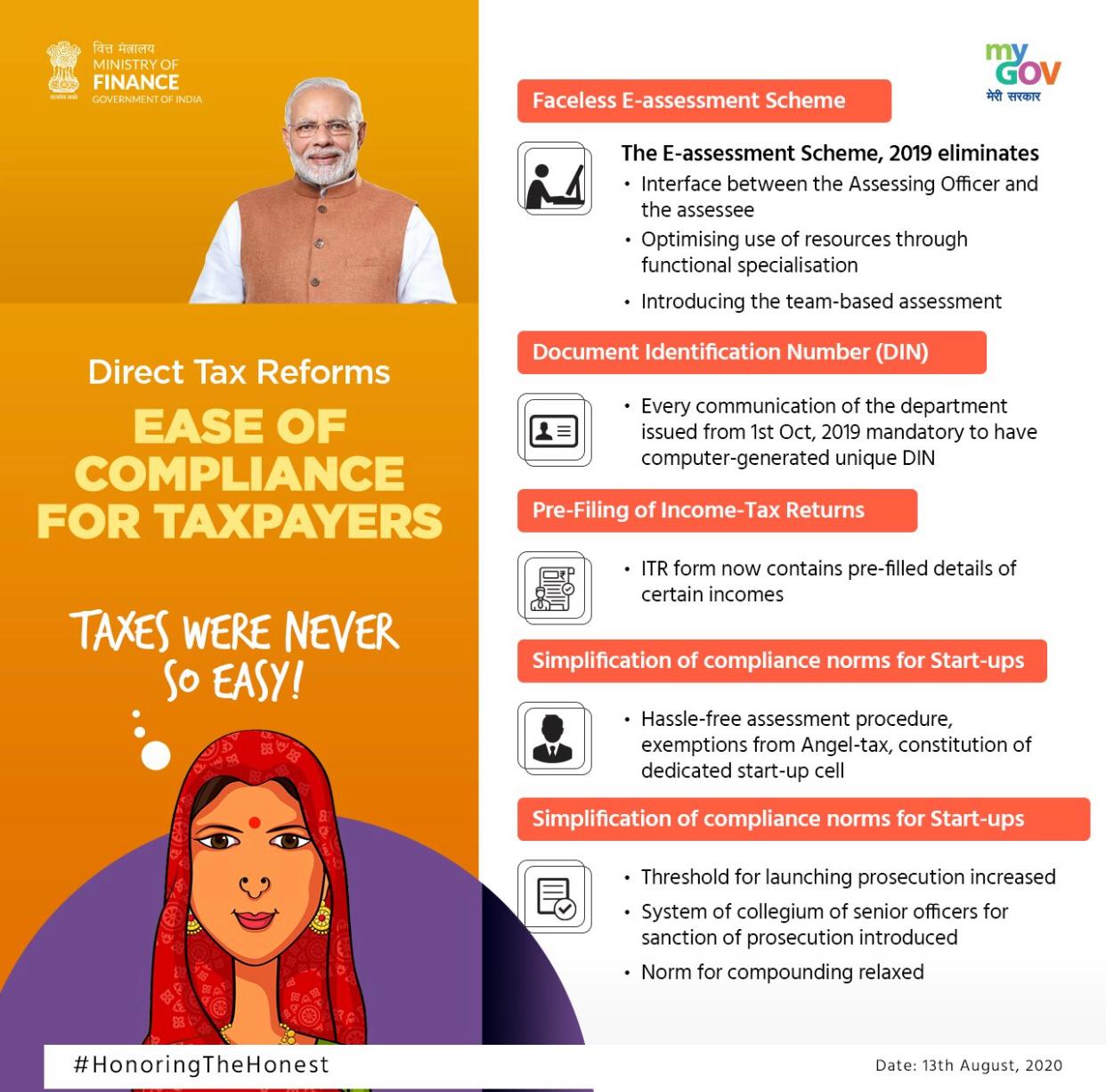

The Income Tax Department has carried out several major tax reforms in the recent years. Last year the Corporate tax rates were reduced from 30 percent to 22 percent and for new manufacturing units the rate was reduced to 15 percent. Dividend distribution Tax was also abolished. Not only has the focus been on reduction in tax rates but also on simplification of direct tax laws. Several initiatives have been taken by the IT Department for bringing in efficiency and transparency in the functioning of the Department. This includes bringing more transparency in official communication through the newly introduced Document Identification Number (DIN) wherein every communication of the Department would carry a computer generated unique document identification number. Similarly, to increase the ease of compliance for taxpayers, IT Department has moved forward with prefilling of income tax returns to make compliance more convenient for individual taxpayers.

With a view to provide for resolution of pending tax disputes the Income Tax Department also brought out the Direct Tax Vivad se Vishwas Act, 2020 under which declarations for settling disputes are being filed currently. To effectively reduce taxpayer grievances / litigation, the monetary thresholds for filing of departmental appeals in various appellate Courts have been raised . IT Department has also undertaken several measures to promote digital transactions and electronic modes of payment. The IT department has also provided relief to taxpayers during the Covid times by extending statutory timeliness for filing returns as also releasing refunds expeditiously to increase liquidity in the hands of taxpayers.

The upcoming launch on Tax Reforms by the Prime Minister will further carry forward the tax reforms in the following areas:.

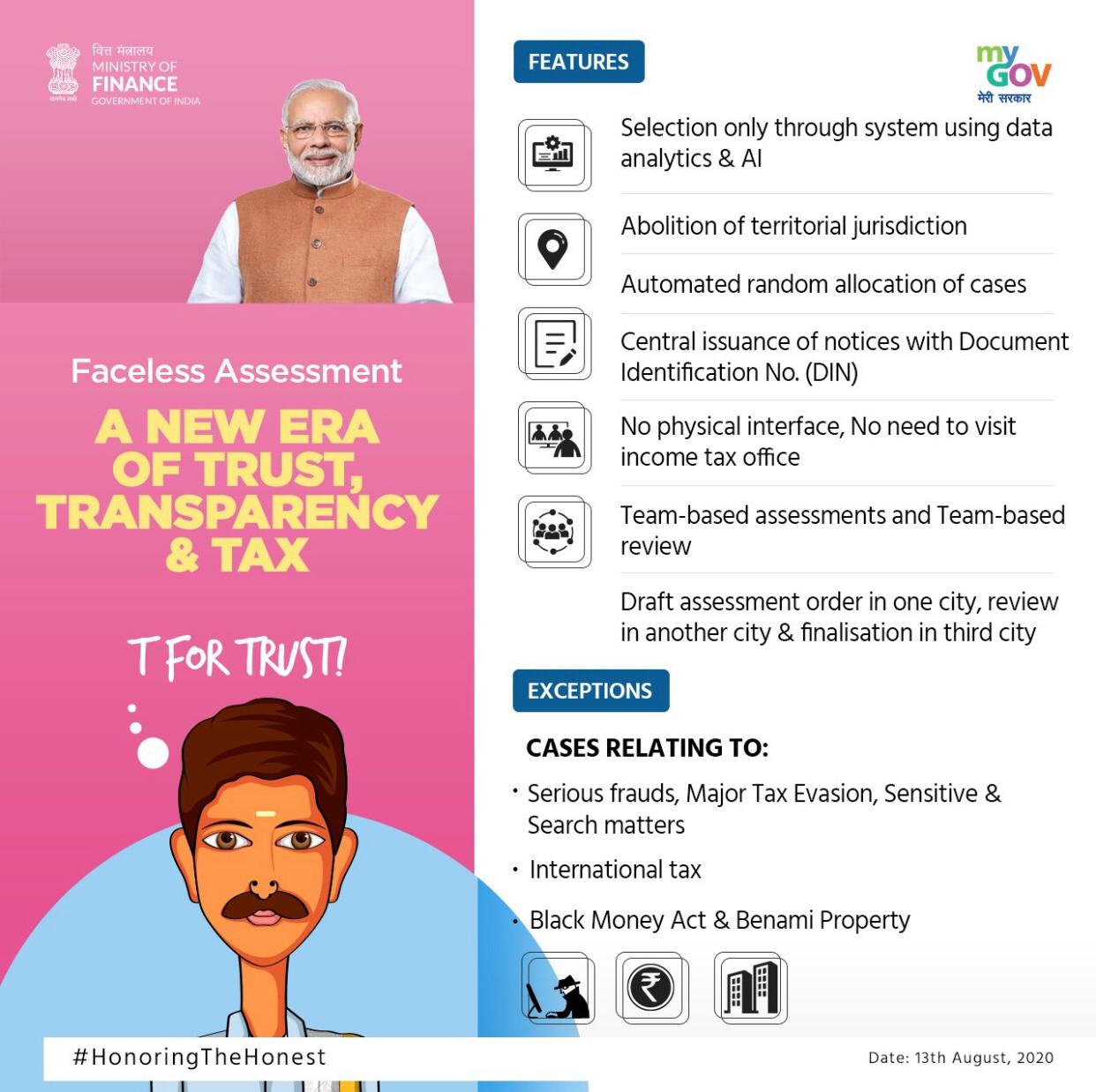

I. Faceless Assessment Scheme – All income tax assessments or scrutiny proceedings except cases of serious frauds, money laundering, cases will done in faceless manner without any physical interface. Therefore, henceforth, any notice or communication pertaining to assessment or scrutiny proceedings received from any Income-tax Authorities other than National e-Assessment Centre (NeAC) would be considered as void or non-est and the taxpayer is not required to comply with any such communication or respond to the same.

The new Faceless Assessment Scheme abolishes age old territorial system of tax administration and assessment. It provides for assessment by randomly chosen virtual teams with dynamic jurisdiction. Assessment is completed through a coordinated effort of various teams viz. Assessment unit, Verification unit, Technical unit and Review unit. The taxpayer is not required at any stage to appear either personally or through authorised representative before any income-tax authority. All communications between the NeAC and the taxpayer are exchanged exclusively through electronic mode. NeAC will randomly assign a case picked up for scrutiny to any assessment unit located anywhere in the country regardless of location of the taxpayer. The Scheme provides for a dynamic jurisdiction under which a taxpayer can be assessed by an officer located anywhere in the country irrespective of his geographical location. Hence, for example, a taxpayer located in Mumbai may be assessed by an assessment unit located in Chennai and verified at Delhi and reviewed at Hyderabad. The Scheme provides for a completely faceless assessment procedure, which is perhaps the first of its kind in the world’s taxation system. Due to its faceless nature, the Scheme will minimise any personal discretion or bias.

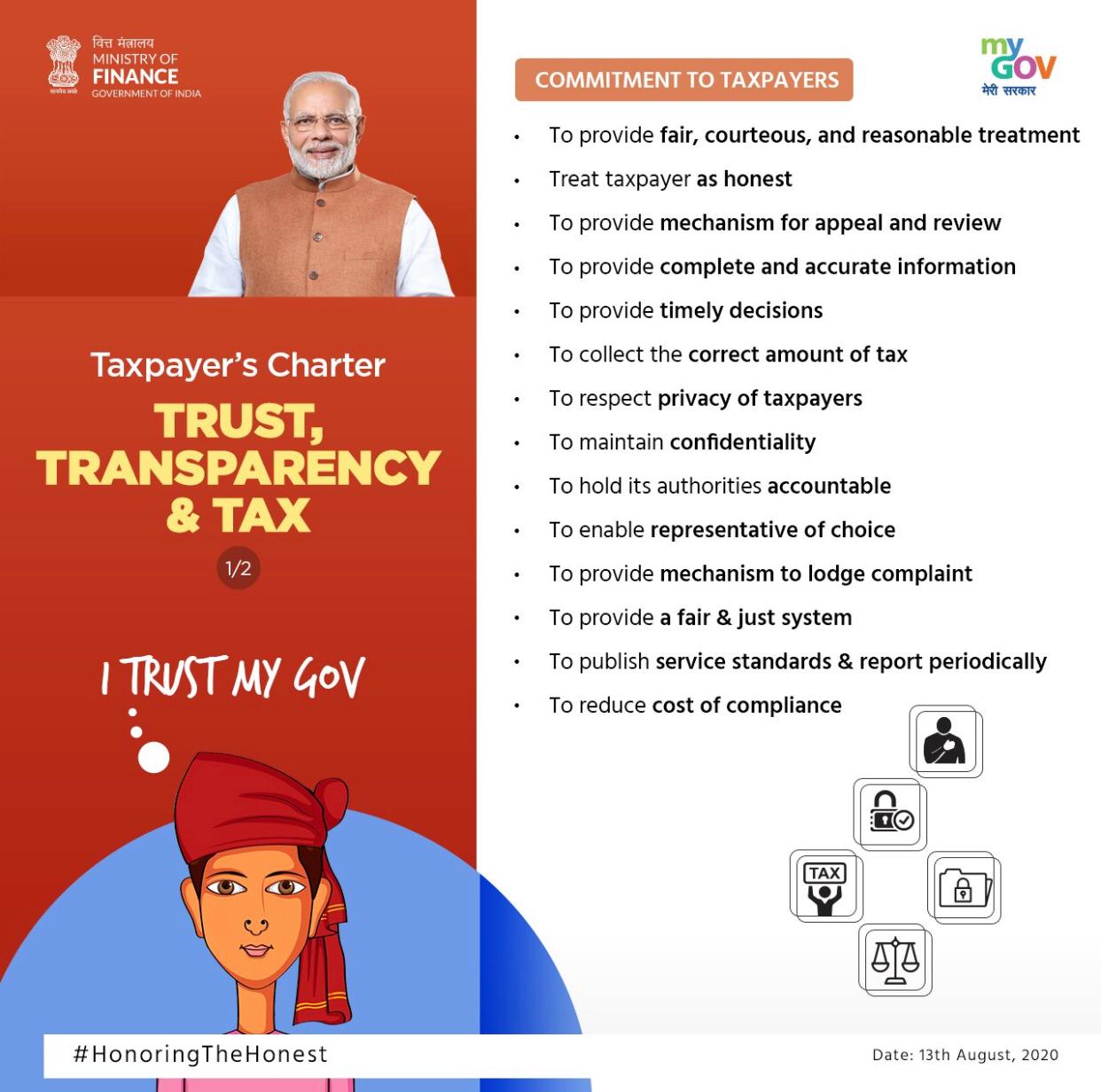

II. Taxpayers’ Charter – The Prime Minister will also launch a ‘Taxpayer’s Charter’. The Charter reflects certain principal commitments of the Income Tax Department towards the taxpayer. With its adoption, India joins other major economies in the world like USA, UK, Canada and Australia which too have adopted and published Charter as a gesture of their commitment towards their taxpayers. The Charter will go a long way in strengthening the trust between the taxpayer and the tax administration. It will also help in enhancing the efficiency of the delivery system of the Income Tax Department.

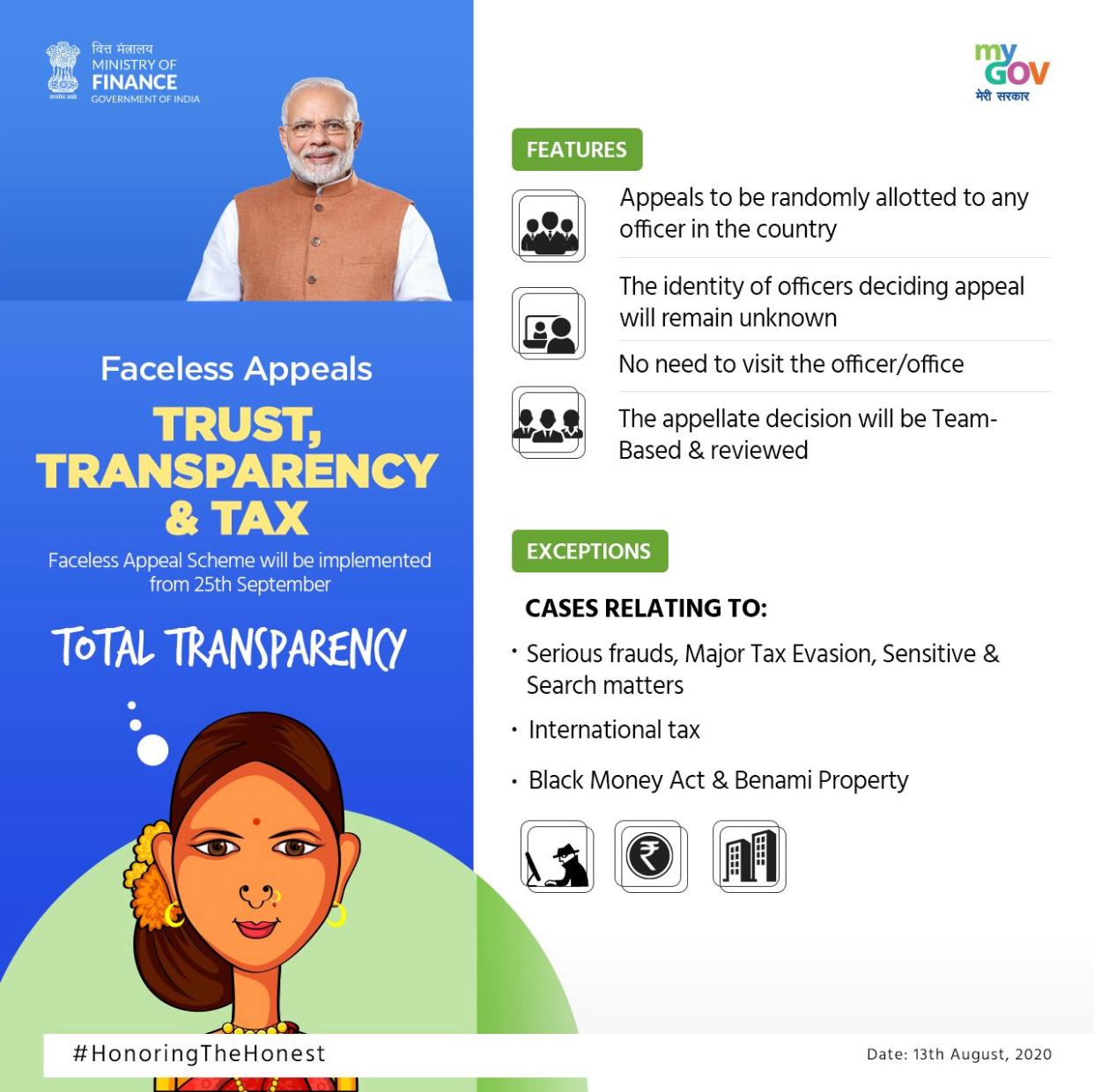

III. Faceless Appeal – Faceless Appeal Scheme shall be implemented from the birth anniversary of Pandit Deen Dayal Upadhyaya i.e. 25th September, 2020. The Scheme will provide a fully faceless procedure for appeals to Commissioner (Appeals) under the Income-tax Act. Like the Faceless Assessment Scheme, it will allow the taxpayers to file their appeals in an electronic mode and thereby save them from the hassles of physically visiting the Income Tax Department. Under this system, the appeal will be heard and disposed by remotely located virtual teams of Commissioners (Appeal). Like faceless assessment, the faceless Scheme too will minimise any bias or subjectivity.

IV. Limiting the intrusive powers of territorial officers to visit business premises- The territorial formations of the Income Tax Department shall no more be permitted to carry out any intrusive action such as surprise visits to the business premises of taxpayers. Intrusive action where specific information on tax evasion is available with the department will be taken only by the TDS Wing or the Directorate of Investigation. Any Survey or visits conducted by any other Income-tax authority barring the above shall be considered as void or illegal.

Other Recent Reforms to attract investments in India

Besides the above measures it may be recalled that earlier the Government had taken a number of measure to reduce tax rates and simplified direct tax laws to facilitate ease of doing business and instil trust in the taxpayers. These measures included -

Reduction in Corporate Tax - Starting from the Finance Act, 2016, the corporate tax rates have been gradually reduced while phasing out the exemptions and incentives available to the corporate. In furtherance of this policy, through Taxation Laws (Amendment) Act, 2019, an option has been provided to the corporate to pay tax at concessional rate of 22% (plus applicable surcharge and cess) if they do not avail any exemption or incentive. Further, new domestic manufacturing companies (set up after 1st October, 2019 and starting manufacture on or before 31st March, 2023) has been provided an option for paying tax at 15% (plus applicable surcharge and cess) without claiming specified exemption and incentive. Further, such companies are not required to pay MAT as well.

Personal Income Tax - Further, in order to reform personal income tax, Finance Act, 2020 has provided an option to individual taxpayers for paying income-tax at lower slab rates if they do not avail specified exemption and incentive. Apart from the above, Finance Act, 2020 has also provided an option to the co-operatives to pay taxes at concessional rates without claiming any specified deduction or incentive.

Attracting Foreign Investment - In addition to structural changes being undertaken in the procedures adopted by the Income-tax Department, recently, several legislative amendments have also been carried out in order to attract foreign investment. Some of the measures taken in this regard by Finance Act, 2020 are as under:

(a) Abolition of Dividend Distribution Tax (DDT): In order to increase the attractiveness of the Indian Equity Market and to provide relief to a large class of investors in whose case dividend income is taxable at the rate lower than the rate of DDT, the Finance Act, 2020 abolished the DDT. In case of a foreign investor, any tax deducted on the dividend can now be availed as credit. Further, such investors can also opt for treaty benefit if such investors are the residents of a country having a Double Taxation Avoidance Agreement (DTAA) with India.

(b) Exemption to Sovereign Wealth Fund (SWF)/ Pension Funds: In order to promote investment of notified Sovereign Wealth Fund (SWF) and notified Pension funds, the interest, dividend and capital gains income of such funds has been exempted from Income-tax subject to fulfilment of certain conditions in respect of investment made in the infrastructure sector. Further to broaden the scope of investment undertaken by these funds, the list of infrastructure has been aligned with the Harmonised Master List of Infrastructure.

(c) Incentive for Offshore Borrowing: The concessional rate of TDS at 5% on interest paid to non-residents on foreign borrowings/bonds and on interest paid to Foreign Institutional Investors (FII) and Qualified Foreign Investors (QFI) specified securities/bonds has been extended to 30th June 2023. Moreover, the concessional rate of TDS has been further reduced to 4% on interest payable in respect of specified bond listed on International Financial Services Centre (IFSC) Stock Exchange.

#####